Context

-

India unveiled the Account Aggregator (AA) network, a financial data-sharing system that could revolutionize investing and credit, giving millions of consumers greater access and control over their financial records and expanding the potential pool of customers for lenders and fintech companies.

-

Account Aggregator empowers the individual with control over their personal financial data, which otherwise remains in silos.

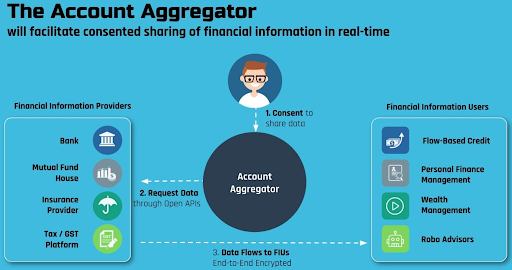

What is an Account Aggregator?

- According to the Reserve Bank of India, an Account Aggregator is a non-banking financial company engaged in the business of providing, under a contract, the service of retrieving or collecting financial information pertaining to its customer.

- It is also engaged in consolidating, organising and presenting such information to the customer or any other financial information user as may be specified by the bank.

- The licence for AAs is issued by the RBI, and the financial sector will have many AAs.

- The AA framework allows customers to avail various financial services from a host of providers on a single portal based on a consent method, under which the consumers can choose what financial data to share and with which entity.

What does an Account Aggregator do?

- It reduces the need for individuals to wait in long bank queues, use Internet banking portals, share their passwords, or seek out physical notarisation to access and share their financial documents.

- An Account Aggregator is a financial utility for secure flow of data controlled by the individual.

How does it work?

- It has a three-tier structure: Account Aggregator, FIP (Financial Information Provider) and FIU (Financial Information User).

- An FIP is the data fiduciary, which holds customers’ data. It can be a bank, NBFC, mutual fund, insurance repository or pension fund repository.

- An FIU consumes the data from an FIP to provide various services to the consumer.

- An FIU is a lending bank that wants access to the borrower’s data to determine if the borrower qualifies for a loan. Banks play a dual role – as an FIP and as an FIU.

- An AA should not support transactions by customers but should ensure appropriate mechanisms for proper customer identification. An AA should share information only with the customer to whom it relates or any other financial information user as authorised by the customer.

What purpose does it serve?

- AA creates secure, digital access to personal data at a time when Covid-19has led to restrictions on physical interaction.

- It reduces the fraud associated with physical data by introducing secure digital signatures and end-to-end encryption for data sharing.

What data can be shared?

- An Account Aggregator allows a customer to transfer his financial information pertaining to various accounts such as banks deposits, equity, mutual fund and pension funds to any entity requiring access to such information.

- There are 19 categories of information that fall under ‘financial information’, besides various other categories relating to banking and investments. For sharing of such information, the FIU is required to initiate a request for consent by way of any platform/app run by the AA.

- Such a request is received by the individual customer through the AA, and the information is shared by the AA, after consent is obtained.

Can an AA see or store data?

- Data transmitted through the AA is encrypted. AAs are not allowed to store, process and sell the customer’s data.

- No financial information accessed by the AA from an FIP should reside with the AA. It should not use the services of a third-party service provider for undertaking the business of account aggregation.

- User authentication credentials of customers relating to accounts with various FIPs shall not be accessed by the AA

Can a consumer decide they don’t want to share data?

- Registering with an AA is fully voluntary for consumers.

- If the bank the consumer is using has joined the network, a person can choose to register on an AA, choose which accounts they want to link, and share their data from one of their accounts for some specific purpose to a new lender or financial institution at the stage of giving ‘consent’ via one of the Account Aggregators.

- A customer can reject a consent to share request at any time.

- If a consumer has accepted to share data in a recurring manner over a period (eg during a loan period), it can also be revoked at any time later as well by the consumer.

Visit Abhiyan PEDIA (One of the Most Followed / Recommended) for UPSC Revisions: Click Here

IAS Abhiyan is now on Telegram: Click on the Below link to Join our Channels to stay Updated

IAS Abhiyan Official: Click Here to Join

For UPSC Mains Value Edition (Facts, Quotes, Best Practices, Case Studies): Click Here to Join